Peninsula Energy: A$60M Capital Raise Set to Finally Bring Lance Into Self-Sufficient Production

- HoldCo Markets

- Nov 20, 2023

- 4 min read

Updated: Feb 13, 2024

DISCLAIMER: Any written content contained herein should be viewed strictly as observation, analysis & opinion and not in any way as investment advice. No compensation was received for this report. Visitors to this site are encouraged to conduct their own due diligence.

Following a halt in trade since the pre-open on November 16, Peninsula Energy finally announced the much anticipated A$60M capital raise (equivalent to ~$39M) which will allow the company to target an initial production re-start for late 2024. The financing comprises A$50M institutional placement to issue 666.7M shares at A$0.075 per share (representing a 37.5% discount from the November 15 closing price) and a A$10M Share Purchase Plan (SPP) to issue 133.3M new shares with attaching options (exercisable at A$0.10 per option) on the same terms as the placement. The options will expire fourteen months from the date of issue.

This capital raise should come as no surprise - the funding requirements were largely telegraphed shortly after Uranium Energy Corp (UEC) unexpectedly announced a toll milling cancellation (details from our July note here), abruptly causing the end to a long standing, mutually beneficial arrangement. Coupled with the existing cash balance ($12.5M) and inventory (210,000 lbs U3O8), the announced financing will allow Peninsula to complete plant construction and the needed wellfield development. Given that Peninsula’s modified re-start plans were unveiled on August 31, fully in-sourced and self-sufficient production from Lance is now expected for late 2024. The capital raise is largely in-line with the estimated re-start budget as announced in late August. Note as well that in order to further facilitate the ramp-up, Peninsula will augment funding with other alternative sources including term debt, working capital facilities, and the potential proceeds from option exercise.

As per construction update, an engineering firm has already been contracted to complete detailed engineering and procurement work for the process plant expansion. Long lead time items for the structure have already been ordered. As per wellfield development, a significant milestone was achieved when it was announced that the installation of the 58-well monitor network in Mine unit 3 (MU3) was recently completed in the Ross production area. Recall that MU3 is expected to be the first production wellfield at Lance. It has been specifically designed for operations using low-pH ISR methods. Note as well that as part of the production re-start program, a drilling program designed to upgrade the remaining Inferred resource within the Kendrick production area has already commenced.

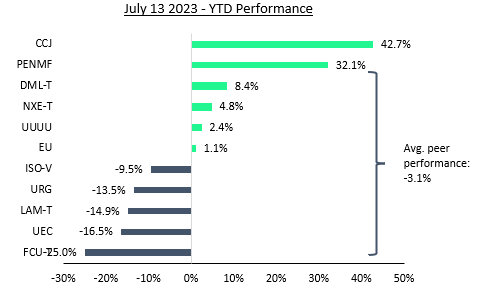

Recall that if not for the unexpected toll milling contract cancellation, Peninsula would have been in production by now already. Moreover, up until the contract cancellation on July 18, Peninsula Energy was in fact leading the way in terms of YTD performance as the market was starting to realize the near and long term ISR capabilities from Lance. As seen below, Peninsula Energy was leading the way in terms of performance among North American peers, ex-Cameco (CCJ):

Now that post-UEC contract cancellation and given that the financing overhang nearly behind us (close expected in early 2024), we would expect Peninsula shares to finally start trading trading in-line with the currently very positive uranium fundamentals, highlighted by a spot price nearing a fresh 15-year high of ~$80/lb. We have previously applauded the decision to fully in-house the entire production value chain and have viewed the decisions taken since contract cancellation as strategically sound for the long term. This comes however with near term pain, a period we are currently navigating through. At this point, we go back to emphasizing the fundamentals, backstopped by the Lance Project which hosts arguably the largest uranium deposit located anywhere in the US. When factoring in the recent Dagger deposit acquisition, the nearly congruent 60.6M lbs (Lance + Dagger) ranks as the second largest uranium deposit located anywhere in the US. In terms of near-term production, Lance alone at 53.8M lbs stands head and shoulders above the rest. Not only is the market still discounting the currently significant size (the current infill program will go a long way to address this concern) but exploration upside remains significant in the very large land package. Based on a combination of past exploration results combined with the currently proposed exploration plan, an exploration target between 104M-163M lbs was previously estimated.

In terms of production, our estimates remain the same as when guidance was provided on August 31. Highlighted by a small-scale production start in late 2024, we see the overall production profile extending until 2034 with a peak of ~1.8M lbs produced per year between 2030-2032. We also stress that the current production plan comprises Kendrick and Ross exclusively. The much larger Barber area, which currently hosts ~30.0M+ Inferred lbs has been completely excluded from the current production plan. We feel that the massive Barber area (representing nearly 75% of the total 8km x 37km Lance acreage) can and will provide the next large pillar of LT production growth. Recall that the Central Processing Facility (built in 2015) is currently licensed for up to 3.0M lbs of dried U3O8 per year. Our current production estimates are presented below:

Our positive thesis remains predicated on our bullish stance on US produced uranium coupled with significant factors which set Peninsula aside from domestic ISR peers – namely, low pH ISR recovery methods (as opposed to the more traditional alkaline recovery), the future resource potential from Barber, the modern CPP + licensed capacity and finally the current team and established track record. Note as well that the company currently has a uranium sales contract book of nearly 5.0M lbs (weighted un-escalated price of $55/lb) extending from now until 2033. The currently contracted lbs comprise up to 34% of the planned LOM production.

While updating for the corporate changes we maintain our 1.20x NAV8% valuation, resulting in a 12-month price objective of $0.18 per fully diluted share, equating to +161% upside from the recent close. Peninsula shares (fully diluted) currently trade at 0.46x NAV8% multiple.