Ahead of the Q3 Earnings, Our Utility Preference Remains on Unregulated Assets with Nuclear Exposure

- HoldCo Markets

- Oct 24, 2022

- 6 min read

Updated: Oct 26, 2022

DISCLAIMER: Any written content contained herein should be viewed strictly as analysis & opinion and not in any way as investment advice. Visitors to this site are encouraged to conduct their own due diligence.

Given the market downturn which has carried on from Q3/2022 and into the start of Q4, we note that markets have seemingly stabilized in the last month as the S&P is flat while the Dow has returned +3.0%. Interestingly enough, the PHLX Utility Index (UTY) is down by over -13.0% in that very same timeframe. We find this disconnect surprising given two main data points:

1) Given the (mostly) regulated nature of utility distribution, transmission and the relatively safe cash flows brought about by LT pricing contracts, utilities have historically had a lower beta to the broader market. Generally, utilities underperform when markets advance and outperform when markets contract. This was evident in FY/2021 when the UTY returned approximately +15% while the broader market S&P500 returned approximately +21%.

2) More recently, following the August 2022 passage of the Inflation Reduction Act (IRA) and with it $369B in clean energy/climate provisions, given the numerous incentives and PTCs/ITCs, we would expect many utilities (namely those with zero carbon footprint generating assets) to outperform. This hasn't quite been the case of late.

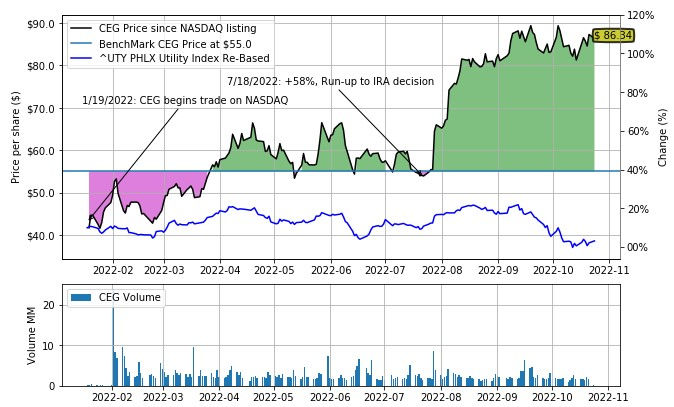

Coincidentally out of the entire utility landscape, Constellation Energy (CEG) is one such company which sticks out - it has advanced by +2.0% in the last month and +59% over the last three months. Following a January 2022 listing, Constellation is one of the largest beneficiaries of the IRA given that it is the largest nuclear reactor operator in US. The PTCs/ITCs contained in the IRA bill provide it with a certain level of price stability for the next 10+ years. Given the level of price stability, another trait we like is the fact that 100% of CEG’s nuclear generating capacity is entirely unregulated. This is another characteristic which separates Constellation from the other utility peers with nuclear generating assets (see below). That said, these are the two traits we prefer to look for when identifying utilities which we would expect to outperform: 1) any amount of nuclear generating capacity and 2) unregulated capacity.

Nuclear IRA Provisions: Though the Inflation Reduction Act provides provisions for wind, solar, hydro, nuclear, natural gas and even hydrogen development/production, nuclear generating capacity is the only one which is both zero carbon and baseload capacity. In short, looking specifically through the nuclear lens, the IRA provides for a maximum credit of $35/MWh at a theoretical power price of $0/MWh. The credit reduces to $0/MWh for power prices exceeding $43.75/MWh given the pricing mechanism is structured as a contract of difference framework. Depending on the company, nuclear generating capacity will have a minimum floor price for (in the least) the 10 next years. This level of certainty will spur both further investments and life extensions for many aging nuclear reactors. Coupled with the fact that natural gas prices have been rising in North America, the IRA pricing floor will ensure that nuclear will once again become economic LT.

Unregulated Capacity: This category comprises Independent Power Producers (IPPs) / merchant generators. These are essentially electric generators with no assigned service territory that produce and sell electricity into wholesale power markets at market based wholesale rates (or based on power sales contracts). This is unlike the regulated utilities which have been granted monopoly power in pre-defined territories, and must sell at state-regulated rates. Another differentiation feature is that traditional regulated utilities usually provide bundled services to consumers – that is generation, transmission, distribution and any other ancillary service. IPPs do not own any transmission assets nor do they sell to retail customers. The concepts between regulated versus unregulated can come down to rate based growth (regulated) versus competitive power (unregulated).

Our current preference for unregulated nuclear utilities stems from the fact that the IRA’s PTCs/ITCs essentially provide the benefits of regulated utilities’ stability and cash flow certainty, without the constraints of being regulated operationally and financially. Unregulated utilities are not as constrained by the heavy burden of regular debt and equity funding required to build and maintain power plants to meet future load growth and offset planned retirements. Growth is much harder as a regulated utility as risk adjusted returns need to be found in a more limited pool of assets found in states with advantageous or incentive based (or supportive) rate making. Every facet of bundled electricity (again, this means generation, transmission, distribution and service) must always be considered as a regulated utility. In addition to pricing upside, unregulated businesses have much more potential M&A upside and have accordingly demonstrated much higher growth rates historically. In our view, the key to a successful utility is relatively simple:

1) Increase capex in order to grow earnings (keep investors happy)

2) Capex spend for resiliency and reliability (keep regulators happy)

3) Minimize opex to keep rates in check (keep consumers happy)

For an unregulated business, point 2 is much less of a concern or burden. As such capex via M&A is much more active. For this reason (and as demonstrated by Constellation’s outperformance over the last three months), unregulated nuclear businesses are now benefitting from cash flow visibility/stability for the next decade+ while also having more options on the M&A front. A second point to keep in mind that any type of fuel needed for baseload electricity generation (be it coal, natural gas or uranium) is not immune to the current inflationary pressures. Uranium however has had much more price stability of late, given an environment in which costs for coal or natural gas have more than doubled in the past year.

In light of our inclination for nuclear generating capacity along with some unregulated assets, our utility preferences include Constellation Energy, NextEra Energy and as a special situation, The Southern Company.

Constellation Energy (CEG): Positive momentum for merchant producers and one of the largest beneficiaries of the IRA. Note that 85% of Constellation’s generation is from nuclear with the balance from efficient natural gas generation in Texas and from renewables. Note that as mentioned before, the nuclear operations are entirely unregulated. The company currently boasts a strong balance sheet for M&A initiatives. The fundamentals remain strong with an expected $2.0B in FCF this year and next. CEG will disclose quarterly earnings on November 8. Q3/2022 EBITDA consensus is for $590M. Expect CEG to address the recent rise in power prices and its strategy to lock in additional hedges at the currently elevated prices. Previous notes can be found here and here.

NextEra Energy (NEE): Is potentially the single largest beneficiary of the IRA. The company enjoys attractive fuel diversity (including nuclear) in its mixed regulated/unregulated business. Q3/2022 earnings will be disclosed on October 28. Until then, the company is guiding towards FY/2022E EPS of $2.80-$2.90 and a 6%-8% LT EPS growth rate. We expect that NEE will provide an update on non-core investments in water treatment, hydrogen, and another clean tech. We also expect an update concerning the company’s transmission investments. The company has been under pressure over the last month, likely due to the ferocity of Hurricane Ian which hit towards the end of September and affected the FPL regulated assets. Recall that Ian was categorized as Florida’s deadliest hurricane since 1935. A previous note can be found here.

The Southern Company (SO): With the Vogtle 3 nuclear load now complete, the company has achieved a major milestone in the process, indicating that the startup of the Unit 3 is now imminent. We believe that this should bring a significant relief to investors who watched in agony the plant’s challenging and protracted construction process over the last decade. Vogtle Unit 3 completion should now de-risk the corporate outlook. Moreover, the Company is on track to finish Unit 4 and move forward with fully reflecting both units in rates. The Southern Company previously estimated an approximately $700M in CFO uplift for FY/2024 once both units are completed and in operation. With Vogtle overhangs diminishing, we believe that management will be freed up to focus on longer term growth targets, possibly involving more M&A. Q3/2022 results will be announced on October 28, consensus calls for Q3 EPS of $1.33. FY guidance is expected between $3.50-$3.60 while the LT growth rate is seen between 5%-7%.