The Month in U Inventory: SPUT & Yellow Cake NAV Updates -Inventories Continue to Grow

- HoldCo Markets

- Mar 1, 2023

- 4 min read

Updated: May 25, 2023

DISCLAIMER: Any written content contained herein should be viewed strictly as analysis & opinion and not in any way as investment advice. No compensation was received for this report. Visitors to this site are encouraged to conduct their own due diligence.

Tradetech reported that the February month end uranium term price ended flat on the month at $52.00/lb, still representing the highest term price since August 2013. As per the spot price, Tradetech reported a February month-end price +$0.10/lb to reach $50.85/lb. February was characterized as yet another active month for adding uranium inventory as SPUT added +1.00M lbs to inventory while Yellow Cake PLC added +1.35M to inventory. Given our LT $70/lb price objective for the spot and a constant CAD/USD exchange rate, our 1.05x NAVPU valuation of $25.70 (rounded) remains for SPUT. For Yellow Cake, assuming the same LT spot price and assuming a constant GBP/USD exchange rate, our 0.95x NAVPU valuation of £620 (rounded) remains. Following a slight premium to NAV at the end of January, we note that SPUT ended the month of February at a -2.1% discount to NAV. Yellowcake’s discount to NAV increased this month to reach the current -8.8% discount.

Activity during the month was driven by news that SPUT updated its ATM equity program to issue up to an additional $1.3B in Trust units. Seeing as the Trust added +1.0M lbs to inventory last month (following the addition of +1.3M lbs in January), the Trust once again played a significant role in buy-side volume. Not to be outdone, Yellow Cake completed a $75M upsized financing during the past month and subsequently purchased +1.35M lbs (at below $50/lb) thus bringing its total uranium to over 20.1M lbs. Note that an option for an additional $100M in purchases from Kazatomprom (KAP) remains open for the remainder of 2023.

On the macro front, eleven EU states vowed to strengthen cooperation on nuclear energy which they said would aid Europe transition away from carbon emitting fossil fuels. Spearheaded by France, the eleven states agreed to support new projects (some of which involve SMRs) alongside existing nuclear power plants. Overseas in the US, three Senators introduced the Nuclear Fuel Security Act – a bipartisan bill which would urge the Department of Energy to establish a nuclear fuel program with the intent of on-shoring fuel production back to the US. This bill follows the House Energy & Commerce Committee's hearing earlier in the month that discussed the introduction of legislation focused on prohibiting the import of low-enriched uranium from Russia. We note that despite the legislation not being signed into law just yet (both laws still require debate and refinement), numerous US based utilities have already been active in self-sanctioning away from Russian origin uranium supply.

Sprott Physical Uranium Trust (U.UN-T, U.U-T): 1-Yr Performance:

Valuation: Given the uranium spot ended the month of February flat at $50.85/lb, SPUT is trading at 0.98x P/NAVPU, or at a -2.1% discount given the current 1.0x NAVPU intrinsic value of $17.26. Note that the valuation premium from the end of January has reverted back to a slight discount. Given our LT $70/lb price objective for the spot and constant CAD/USD exchange rate, our 1.05x NAVPU valuation of $25.70 remains. For context, the current -2.1% discount to NAVPU is relative to +26% premium in September 2021 and -18% discount from July 2022. At the peak 2022 spot price of $63.88/lb on April 13, units traded at a modest -5% discount. The corresponding sensitivities to FX and the spot price are below:

We feel that SPUT's -2.1% discount to NAV is justified when compared to Yellow Cake's current -8.8% discount to NAV. We stress that in addition to higher liquidity and inventory, SPUT stores all of its physical uranium inventory at facilities owned and operated by Cameco (Canada), ConverDyn (US) and Orano (France). Unlike Yellow Cake, SPUT has much less direct exposure to sourced uranium from Kazakhstan.

Yellow Cake plc (YCA-L): 1-Yr Performance:

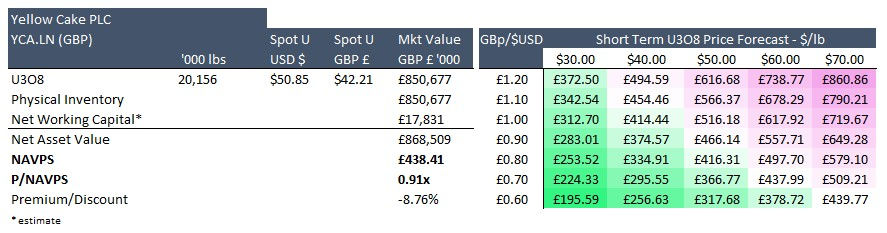

Valuation: Given the most recent spot U3O8 quote at $50.85/lb (or £42.21/lb), YCA is trading at 0.91x P/NAVPU, or at an -8.8% discount given the current 1.0x NAVPU intrinsic value of £438.41. Yellow Cake normally trades at a discount to intrinsic value relative to SPUT, justifiably reflecting the smaller size, liquidity and larger perceived delivery risk associated with Kazakh sourced uranium. This dynamic is currently being reflected. Given our LT $70/lb price objective for the spot and a constant GBP/USD foreign exchange rate, our 0.95x NAVPU valuation of £620 remains. The corresponding sensitivities to FX and the spot price are below:

Recall that Yellow Cake has a long term supply agreement with Kazatomprom with the right to purchase $100M worth of U3O8 every year (at spot). On back of Kazatomprom's recent production guidance reduction and logistical transport challenges which partly led to lower quarterly volumes, geo-politics will continue to weigh on Kazakh sourced uranium, and in general on all companies with exposure to Kazakhstan, (despite transport routes which completely bypass Russia).