Fortune Bay Corp. (FOR): The Advanced-Stage GoldFields Project is Worth Watching

- HoldCo Markets

- Feb 4

- 16 min read

DISCLAIMER: Any written content contained herein should be viewed strictly as analysis & opinion and not in any way as investment advice. Visitors to this site are encouraged to conduct their own due diligence. As a Research Spotlight product, HoldCo Markets has received financial compensation for the written content and analysis below. Please read the full disclaimer here: holdcomarkets.com/disclaimer

We are initiating coverage of Fortune Bay Corp. (FOR) with a 12-month price objective of C$3.15 per share. Boasting an attractive PEA stage Project (Goldfields), we expect a lot of news flow on the development front over the next few months on the way to an eventual PFS expected by year-end or Q1/2027. Though much of Fortune Bay’s previous history has been tied to uranium exploration, following a change in strategic direction, 2026 will mark the company’s first full year as a pure-play gold company. As the story becomes better known and as development milestones are met at Goldfields, we see plenty of potential for a company re-rate in valuation.

COMPANY OVERVIEW

Headquartered out of Halifax, Nova Scotia, Fortune Bay Corp. is a Canadian focused exploration & development mining company, listed on both the TSX Venture Exchange (Symbol FOR), on the Frankfurt Stock Exchange (5QN) and on the OTCQB in the United States (FTBYF). Located on the northern shore of Lake Athabasca in northern Saskatchewan, the flagship Project is the past-producing Goldfields Project. Though permitting and environmental baseline studies are on-going along the road to an eventual Pre-Feasibility Study, the company remains aggressive with exploration drilling as well. Specifically, a 3,250m drilling program (encompassing 17 drill holes) is currently underway on the project with multiple targets identified at both current deposit areas and on underexplored areas with recorded historical occurrences.

HISTORICAL GOLD PRODUCTION

Gold was first discovered on the Goldfields Project in 1934 with Cominco subsequently acquiring the discovery by staking claims. Between 1934-1942, both the Box and Athona deposits were explored and delineated with surface and underground drilling. Horizontally oriented underground core drilling was carried out to intersect gold-bearing quartz veins and crosscuts were driven at each shaft station and along certain underground drill holes to check analytical results. Stope and mill development continued during a period between 1936-1938. Production from underground operations began in June 1939 at 450 tpd, with capacity ramping up to a maximum of 1,100 tpd in 1940. Ultimately, a total of 64,000 gold ounces was produced from the Box deposit until a labor shortage prompted the cessation of mining and development work in 1942. At time of production, gold grades were estimated to be 1.71 g/t with recoveries ranging between 92%-96%. Later on, uranium-focused exploration (airborne radiometric, ground geophysics, mapping, and drilling) was carried out until the late 1980’s. Additional phases of delineation drilling in support of gold resource estimation were carried out at Box and Athona during the period 1988 to 2011, at which point almost 750 surface and underground delineation drill holes had been completed with a gold assay database including over 35,000 results.

More recently, In May of 2009, Linear Gold Corp. acquired the Box and Athona properties through its subsidiary 7153945 Canada Ltd. In June of 2010, a merger between Linear and Apollo Gold Corp. formed Brigus Gold Corp. In December 2013, Brigus was acquired by Primero Mining Corp. and the Goldfields project was spun out into Fortune Bay Corp. 7153945 Canada Ltd is now a wholly-owned subsidiary of Fortune Bay.

GOLDFIELDS PROPERTY LOCATION & INFRASTRUCTURE

The Goldfields Project currently consist of 14 mineral dispositions covering a total surface area of 5,923 ha. The Project is located 850km north of Saskatoon or 12 km south-southeast of the town of Uranium City in northern Saskatchewan (60 km south of the border with the Northwest Territories). The Goldfields Project contains at least 5 mineral deposits or occurrences that reached significant underground exploration stages (Frontier Lake, Golden Pond, Triangle, Nicholson Bay and Fish Hook Bay) and 2 that reached the stage of mine development and production (Box and Athona).

The Project itself is accessible by vehicle via the partially maintained gravel Highway 962 from Uranium City and subsequent historical trails to the Box and Athona deposits. Scheduled commercial flights are available to Uranium City three or four times per week from Saskatoon, which also provide connections to other northern communities in Saskatchewan. The Box and Athona deposits are located on the northern shore of Lake Athabasca and are accessible by boat or barge in the summer months. The Project also directly overlies the seasonal winter ice road that crosses Lake Athabasca between Uranium City and Stony Rapids.

GOLD MINERALIZATION

The Box and Athona deposits, located 2 km apart, share many similarities which suggest a close genetic association. Mineralization characteristics at Box and Athona are similar, comprising quartz vein sets hosted within a metamorphosed and hematized leucogranite, respectively termed the Box and Athona “Mine Granites”. The gold mineralization at Box and Athona is associated with quartz veining which shows preferred structural orientations. Gold-bearing quartz veins vary in true thickness from >50 cm down to sub-centimeter size. Thicker vein sets have been shown during historical mining to be continuous up to lengths of over 100m. At Athona, mineralization is predominantly hosted in vein sets striking north, steeply dipping (>75°) to both the east and west. Mineralization at both the Box and Athona deposits is strongly structurally controlled and associated with a network of milky white quartz veins that have an average N-S trend and moderate to steep westerly dips. The Box and Athona gold mineralization shows many characteristics which support their classification as orogenic gold deposits. These include a regional association with an orogenic fold belt (Trans-Hudson Orogen), quartz-vein or fracture dominated mineralized material systems within a brittle structural regime, and association with sulphides (albeit very low levels <0.5%).

HISTORIC EXPLORATION

Extensive work was conducted on the Project between 1934-1942. The project lay dormant until the 1980s when trenching, prospecting, metallurgy sampling and resource delineation was re-started on site. GLR took ownership of the Project in the mid 1990s and followed up with additional mapping, sampling and airborne geophysical surveys. Up until ownership from Brigus Gold, the more recent work on site involved drill testing targets at Box, Athona, Frontier Lake and Triangle. Up until 2011, historic drilling at Athona totaled 376 drill holes totaling 29,077m while at Box, historic drilling amounted to 552 drill holes totaling 67,108m.

RECENT DRILLING

As per more recent drilling by Fortune Bay, 18 holes (6,946m) were drilled at Goldfields between January 2021-March 2022. The drilling was focused at Athona and Box. The program was specifically designed to expand the mineralization footprints beyond the historical drilling coverage, and to commence delineation of additional mineral resources. Post-drilling, a total of 3,036 samples were collected and submitted for gold assay and analysis. Highlight assays from both Athona and Box included:

A21-218: 3.0m grading 3.60 g/t Au from 115.0m to 118.0m (Athona)

A21-221: 2.0m grading 1.57 g/t Au from 32.0m to 34.0m (Athona)

A21-223: 19.0m grading 1.22 g/t Au from 92.0m to 111.0m (Athona)

B21-334: 8.0m grading 4.38 g/t Au from 286.0m to 294.0m (Box)

B21-335: 36.0m grading 1.34 g/t Au from 312.0m to 348.0m (Box)

B21-338: 19.0m grading 1.42 g/t Au from 413.0m to 432.0m (Box)

All samples from Box and Athona were incorporated into the mineral resource estimate. From Athona, holes A21-219, A21-220 and A21-222 all intersected mineralization, demonstrating expansion of Athona to the south. Drill holes A21-218 and A21-221 intersected grades and mineralization characteristics consistent with those observed within the Athona Main deposit, suggesting continuity between Athona Main and Athona South. From Box, results for drill holes B21-334 to B21-340 represented a significant expansion of mineralization, including up to 280 m down-dip from the previous 2021 mineral resource estimate and 100m down-dip of mineralization intersected previously across the strike of the deposit. Locations of the Bulk Density Samples below:

GOLDFIELDS MINERAL RESOURCE ESTIMATE

The primary host lithologies to the mineralization are the Box (BMG) and Athona (AMG) granites, the modelled volumes also represent the main resource domains bounded by relatively unmineralized footwall and hanging wall lithological domains. To further constrain the mineralization within the BMG and AMG domains, a vein system model was generated within each of the granite domains. This was achieved using a combination of the Vein Modelling and Economic Compositing Tool in Leapfrog GeoTM. Gold assay data intercepts were composited using the Economic compositing tool to a grade of 3 g/t and a minimum mineralized material composite width of 0.5 m Assay samples were composited to a 1.5m fixed length to ensure that all data were evenly weighted for block grade interpolation. Over 90% of assay samples were collected using a 1.5 m sample length or smaller, and therefore supported a 1.5 m composite length. Separate block models were generated for the Box and Athona deposits. Block models for Box and Athona used sub-blocking at a 1x2.5x1 m and 1x1x1m sub-block resolution, respectively, to ensure accurate volumetric reporting. Grade interpolation was conducted at the parent block size of 5x5x5m. Block model validation was conducted using multiple techniques including:

Visual inspection of estimated block grades relative to composite grades.

Swath plot analysis of grade profiles between the ordinary-kriged (OK) and nearest-neighbour (NN) block estimates.

Statistical comparison of global average estimated block grades and composite grades, per estimation domain; and

Estimation parameter sensitivity analysis and historical production reconciliation.

Deposit swath plot comparison of Au (g/t) grade for OK and NN Block Models below:

The latest NI43-101 compliant Mineral Resource Estimate models (replacing the MRE with an effective date of October 31, 2022) included a total of 838 boreholes, of which 494 are located within the Box deposit and 344 within the Athona deposit. Gold grades were interpolated into the block models using ordinary kriging (OK) for all granite and vein-set domains within the Box and Athona deposits. Grade estimation for each domain was conducted using multiple passes, with successively expanding search criteria in subsequent estimation passes.

Ultimately, both the Box and Athona deposits remain open at depth. Exploration drilling began this past November at the Box deposit with 3 holes completed totaling 1,125m. At Box, current drilling is focused on down-dip step-outs (200m-350m) into significant gaps in drill coverage within and below current Inferred Mineral Resources, well outside of the mine pit outlined in the updated PEA. A total of 17 drill holes (3,250m) are planned for this winter split between Box (4 total holes) and Athona (2 holes). Additionally, exploration drilling will also focus on targets such as Frontier (3 drill holes planned for), Golden Pond (six holes) and Triangle (2 holes).

The PEA process design is based on treating mineralized material from the Box and Athona open pit mines through leaching and gravity extraction to produce gold doré bars. Note that the PEA is based on a subset of mineral resources comprising 97% of the Indicated mineral resource along with 3% of the Inferred mineral resource. The key production parameters (derived from test work conducted at SGS in 2015) include:

Nominal throughput of 4,950 t/d or 1.8 Mt/a

Crushing plant availability of 65%

Plant availability of 92% for grinding, leach plant and gold recovery circuits.

Plant design grade of 1.9 g/t gold with an allowance to accommodate feed grade variations.

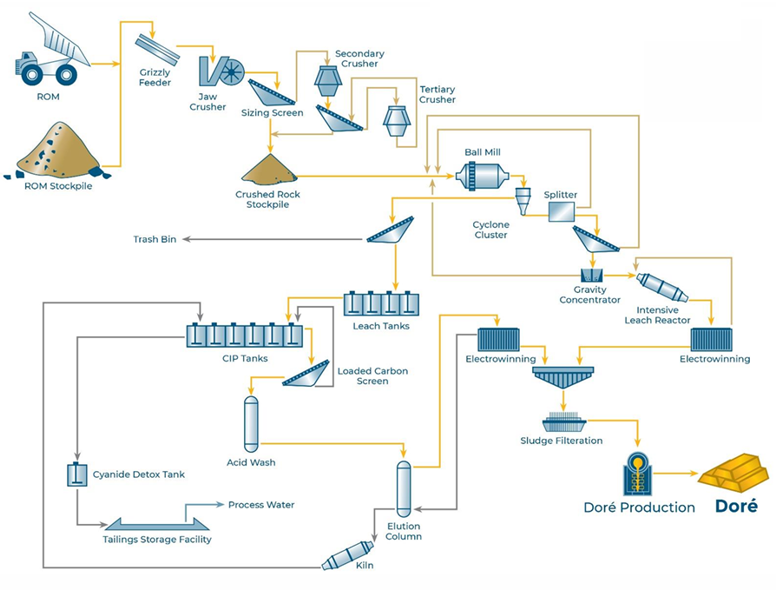

The updated 2025 PEA mine plan incorporates a resource base amounting to 97% of the current Goldfields Indicated resource. Production is outlined as a conventional open-pit mining project with on-site gold recovery at a 4,950 tpd (1.8 Mt/a) processing facility. The process facility is to house milling, gravity, leaching and CIP tanks and the carbon acid wash and elution circuit. The facility is divided into four sections. The first section will contain the mill cyclone cluster and gravity concentrator; the second will contain the leaching, CIP, and water tanks. The third section consists of the carbon acid wash and elution area. Finally, a fourth area will consist of the gold room. Material is hauled from the mine and tipped either directly into the primary crusher ROM hopper or to the stockpile.

As outlined in the PEA, material from the ROM hopper is passed through a vibrating grizzly feeder and oversize is crushed by the primary jaw crusher. The primary crusher product is discharged with the grizzly undersize and conveyed to the secondary screen. The grinding circuit consists of a ball mill in closed circuit with classifying hydrocyclones. The ball mill slurry discharges through a trommel where the undersize discharges into the cyclone feed pumpbox. Gravity tailings are also discharged to the cyclone feed pumpbox. Feed to the gravity circuit is pumped from the cyclone feed pumpbox to the scalping screen via a dedicated pump. Concentrate from the gravity circuit reports to the intensive leach reactor (ILR). ILR solution is made up within the heated reactor vessel feed tank. The reagent mixture is pumped to the bottom of the ILR cone producing a fluidized bed. Overflow returns to the solution tank. The pregnant leach solution is pumped to the gold room for electrowinning and refining. The mine production schedule is envisioned below (Moose mountain, 2025):

PEA ECONOMICS

Given a forecast 4,950 tpd throughput, the mine life was calculated at 13.9 years including 11 years of direct mill feed from pit operations and subsequent low-grade stockpile rehandling. Over the entire project LOM, total payable gold production was estimated to be 896,000 ounces, or 64,300 ounces per year on average. Factoring in a cash cost of $1,207 per ounce ($1,330 per ounce AISC), initial capex of C$301.1M and sustaining capex of C$142.5M, (among others). Using a base case LT gold price deck of $2,600 per ounce, an after-tax NPV5% of $913.7M was calculated, along with an after-tax IRR of 44%. At a LT gold price of $3,650 per ounce, the after-tax NPV5% amounted to $1,253M while the after-tax IRR totaled 74.2%.

HCM GOLDFIELDS ESTIMATES

As per our own estimates for Goldfields, we are cognizant of the ~92% increase in the spot gold price since the base case of $2,600 was used for the PEA (or ~37% increase from the PEA upside scenario of $3,650 per ounce). Given gold’s meteoric rise in such a short time frame, using an appropriate LT price is paramount to our modeling. Depending on one’s viewpoint, our base case of $4,000 per ounce can be seen as either aggressive or conservative given that the current spot at $5,030 per ounce. For context, just ~four months ago when the PEA was released, spot gold was ~$3700 per ounce. That said, we provide a degree of price sensitivities ranging from $3,000 per ounce to $5,000 per ounce.

For our production estimates, we don’t stray that far from the PEA however we do factor in slightly lower throughput and recoveries. Elsewhere, we factor in a degree of cost inflation relative to the figures in the PEA. Our initial capex figure is set to $380M (+27% relative to the PEA) while our average over LOM cash cost per ounce produced and AISC are +45% and +50% respectively, relative to the PEA figures. Sustaining capex is also adjusted +40% higher.

As can be seen above, note that the last three years of production will be exclusively sourced from stockpiled material. The details Goldfields sensitivities can be seen later in the Valuation section below.

POMA ROSA

Located in Chiapas State in southern Mexico, the wholly-owned Poma Rosa property (formerly known as the Ixhuatan property) is a copper-gold project which includes a historical gold resource and large scale growth potential. The property is located in the north-western portion of Chiapas State approximately 100km south of the city of Villahermosa, the capital of Tabasco State. Chiapas is the southern-most state in the Mexican Republic, bordering on Guatemala to the southeast, with the Mexican states of Tabasco to the north; Oaxaca and Veracruz to the west and the Pacific Ocean to the south west. The main part of the property (the Campamento deposit) is located 3 km to the west of the town of Tapilula on highway 195. The Poma Rosa project consists of the 4,176 hectare Rio Negro concession which is valid until May 10, 2051.

Extensive exploration and drilling conducted between 2000-2009 by M.I.M. Mexico S.A. de C.V., Linear Gold Corp. and Kinross Gold led to detailed geological, geochemical and geophysical surveys for the property. Moreover, 89,000m was drilled spread over 342 drill holes. This work led to the discovery of several mineralized zones including the Campamento epithermal deposit, the Cerro La Mina porphyry prospect and numerous other surface prospects. Cerro La Mina was the focus for much of Kinross’ exploration on the property. The best drill intercept came from hole IXCM08-51 which graded 0.68 g/t Au, 2.71 g/t Ag, 2802 ppm Cu and 288 ppm Mo over 601.4 m, from 1.45 m to 602.9m.

In 2011 a NI43-101 compliant resource estimate was completed (prepared for Canagold Ltd.) outlining an estimated 1.04M gold ounces and 4.4M silver ounces in the Measured & Indicated category along with an estimated 0.70M gold ounces and 2.26M silver ounces in the Inferred category.

Carbonate-base metal gold mineralization at the Campamento deposit consists of a stockwork of several types of veinlets hosted in andesitic fragmental rocks. Veinlets are quartz-poor and dominated by carbonate, likely a high manganese variety (kutnahorite) as suggested by the strong manganese staining of surface exposures. Gold and silver mineralization occurs with base metals in veinlets and as wall rock disseminations.

Poma Rosa’s copper potential can’t be understated as it sits on a geological setting which parallels the majority of the giant porphyry deposits worldwide, including shallowly-dipping subduction of an aseismic ridge with associated igneous alkalic rocks similar to those hosting such deposits as Grasberg (Indonesia), Bingham Canyon (USA), Cobre Panama (Panama) and Cascabel (Ecuador). Below, identified gold opportunities (left) and underexplored copper potential (right).

Almost all drill holes to date have intersected gold/copper mineralization. Though previous exploration focused largely on gold, strong copper mineralization at Cerro La Mina, Caracol and Santa Fe indicate the potential for a large district-scale Cu-Au-Ag-Mo mineralized system as well.

Santa Fe skarn: 0.6% Cu, 2.4% g/t Au, 120 g/t Ag and 1.30% Pb

Cerro La Mina: 601.4m grading 0.28% Cu, 0.68 g/t Au, 2.71 g/t Ag (0.9% CuEq)

Campamento: 100.0m grading 12.0 g/t Au and 64 g/t Ag

Western Zone: 140.0m grading 0.70 g/t Au and 0.9 g/t Ag

Laguna Grande: 56.0m grading 1.5 g/t Au and 1.7 g/t Ag

Though there has not been much significant work completed on site since 2009, management was successful in advancing stakeholder engagement and support for the Poma Rosa Project last year. Various initiatives included substantive discussion and negotiation with local landowners regarding exploration agreements which would support the resumption of field-based exploration activities. On November 19, 2025, the Government of the State of Chiapas published a decree establishing a state-level protected natural area known as the Zona Sujeta a Conservación Ecológica “Mina Banderas”, located in the Municipality of Pantepec. Based on recent review of the decree and associated mapping, a portion of the designated area overlaps with the Company’s Rio Negro concession, which remains valid and in good standing under federal Mexican mining law.

The overlapping area covers ~11% of the Rio Negro concession and includes a portion of the Campamento gold-silver deposit and other nearby exploration target areas. Management continues to work closely with Mexican legal counsel to assess the scope and implications of the decree and the amparo process.

PARTNER-FUNDED URANIUM PORTFOLIO

Murmac and Strike Projects

Located on the northern rim of Saskatchewan’s prolific Athabasca Basin, the Murmac and Strike projects comprise 21 mineral claims covering an area of ~20,000 hectares located within 25km of Uranium City. Work at both project areas is currently being funded by Aero Energy Ltd (AERO) under an option agreement executed on December 15, 2023. The agreement provides for a 70% earn-in subject to exploration expenditure of C$6.0M over a 3.5 year time period.

Previous work conducted by Fortune Bay included 36 competed drill holes totaling 7,654m. Targeting defined electro-magnetic (EM) conductors, the most encouraging drill result to date is an intercept at Murmac of 0.3% U3O8 over 8.4m with individual assay grades up to 13.8% U3O8 (discovery drill hole M24-017). Anomalous uranium (defined as >100 ppm U) was intercepted in 13 of the 32 holes for which geochemical results were available.

The geological setting, historical datasets and current drill results support the project’s potential for Athabasca Basin high-grade unconformity-related, basement-hosted uranium deposits. The targeted drilling on the Murmac property is located ~10km east of the historic Gunnar Mine which accounted for 18M lbs of historic uranium production. As announced on December 30, 2025, Aero Energy closed the final tranche of a non-brokered private placement for gross proceeds of C$5.0M.

The Woods

The Aspen, Birch, Fir, Pine and Spruce projects (known collectively as The Woods), comprise 25 separate dispositions covering 41,000 hectares. The projects are located within 30 km of the northern Athabasca Basin margin and overlie a significant portion of the strike length of the Grease River Shear Zone (GRSZ), a major structural feature that is significantly underexplored in comparison with other major Athabasca Basin structures. As announced on July 30th 2025, Fortune Bay entered into a definitive option agreement (dated July 25, 2025) with Neu Horizon Uranium Ltd, a private Australian arms-length party. The option agreement provides for an 80% earn-in subject to exploration expenditures of A$3.0M over a 1.5 year time period.

The Woods Projects display favorable geological settings and structural features for both uranium and REE mineralization. Historical exploration activities identified a significant uranium endowment in the area, including numerous uranium occurrences of vein- and pegmatite-hosted mineralization indicating potential for both basement-hosted and Rössing-style (ie lower grade yet near surface) deposits.

As announced on December 10, 2025, New Horizon Uranium completed a capital raise for $500,000 and continues to plan for a Q1/2026 listing on the ASX. The completion of modeling and interpretation of the recently flown VTEM geophysical survey and the defining of high priority, basement hosted uranium targets along the GRSZ will be the priorities for Neu Horizon. Along with ground physics and mapping, establishing drill-ready targets for an actual drilling program are the initiatives envisioned following the ASX listing.

PEER VALUATION

For comparative purposes, we assembled a peer group of North American gold development projects ranging from Quebec to the Yukon and extending as far south to Nevada and Utah (among others). Though the individual peer group projects vary in terms of development and de-risking, most of the projects listed below have a relatively recent PEA or PFS technical study. In the very least, a relatively recent MRE has been published (this is the case for Bonterra Resources, Sitka Gold, Maple Gold and Lafleur Minerals).

As can be seen from the exhibit above, though Fortune Bay ‘s Goldfields project ranks among one the smaller deposits given a current global resource of 1.2M gold ounces, this fact is reflected in the current enterprise value which accordingly, ranks among the lower echelon on the peer group. Fortune Bay is currently trading at a $58 per ounce EV valuation given the current 1.2M lb global resource from the Goldfields Project. This is at a near ~40% discount relative to the peer group trading at a valuation of $92 per ounce. We feel that given the current 3,250 drilling campaign, the risk remains on the upside for resource growth at Goldfields. Additionally, the fact that management is targeting a PFS for Q4/2026 or Q1/2027, we feel that as the de-risking work continues, the corporate valuation will re-rate as the story is told and as development milestones are met.

VALUATION & CONCLUSION

As per our company wide valuation, we value Goldfields using a base case, LT gold price of $4,000 per ounce using the parameters specified earlier in this report. For Poma Rosa, acknowledging the early stage nature of the project coupled with the current project situation requiring clarity in Mexico, we apply a $100 per ounce in-situ valuation to 70% of the historically defined Measured & Indicated resource (1.04M Au ounces). Factoring in a partial future equity financing (post-PFS provided a positive FID), we derive a 12-month price objective of C$3.15 per share by applying a 0.20x NAV8% multiple. Given the most recent close (February 3rd), shares of Fortune Bay currently trade at a 0.06x P/NAV multiple. As mentioned, Fortune Bay also trades at an attractive EV $58 per ounce multiple versus the peer group. Acknowledging the acute sensitivities to the LT gold price (below), our price objective equates to upside of +242% from the most recent close.

We are excited with Fortune Bay’s prospects this year and note that 2026 will be the first year in which the company should potentially re-rate to being viewed as a pure-play gold company with an advanced project working towards PFS completion by year-end. Recall that in previous years, the company was considered as a uranium exploration company focused primarily on the Murmac uranium project. We expect material news flow to trickle out from the winter drill program at Goldfields. Recall that the current drill program also includes several exploration targets. With a PFS expected to be competed by year-end or Q1/2027, as the story becomes more familiar to the market, we would expect this company to re-rate to similar valuation metrics as seen with the North American Peer group. Given the most recent close (February 3), shares of Fortune Bay currently trade at a 0.06x P/NAV valuation, or at $58 per global Au ounce – well below that of peers.

NEAR-TERM TIMELINE & POTENTIAL CATALYSTS

Drill results from the current 3,250m program at Goldfields. Details for a Summer program.

Metallurgical and Geotech results over the course of the year.

Goldfields PFS details leading up to an actual study scheduled for year-end or Q1/2027.