Pre-PDAC Company Updates: Our Best Ideas Across Uranium, Copper & Precious Metals

- HoldCo Markets

- 31 minutes ago

- 19 min read

DISCLAIMER: Any written content contained herein should be viewed strictly as analysis & opinion and not in any way as investment advice. Visitors to this site are encouraged to conduct their own due diligence. As a Research Spotlight product, HoldCo Markets has received financial compensation for the written content and analysis below. Please read the full disclaimer here: holdcomarkets.com/disclaimer

Though markets have been a shade above flat YTD, commodities have continued with their torrid pace upwards as gold, silver, copper and uranium have increased by +22%, +34%, +7% and +7% respectively, YTD. Ahead of the annual Prospectors & Developers Association of Canada’s (PDAC) annual mining convention in Toronto (March 1-4), we highlight our current best ideas in the mining sector spanning the uranium, copper and precious metals space. We highlight five companies specifically:

Myriad Uranium Corp (M)

Copper Fox Metals Inc (CUU)

Fortune Bay Corp (FOR)

Premier American Uranium Inc (PUR)

Terra Clean Energy Corp (TCEC)

Given elevated pricing and an environment which has become much more conducive to drilling and development (as evidenced by the Fast-41 permitting initiatives, the creation of incentives for critical minerals extraction and various provincial permitting initiatives) we continue to favor two particular items when sifting though company prospectuses, technical reports or quarterly operating results:

1) Our preference is for a geographic project location in either the US or Canada and

2) We prefer projects which have either an extensive history of past production or have an extensive history of past drilling, along with the accompanying technical reports and data.

In addition to accomplished management teams, all the companies mentioned above fit well given our criteria.

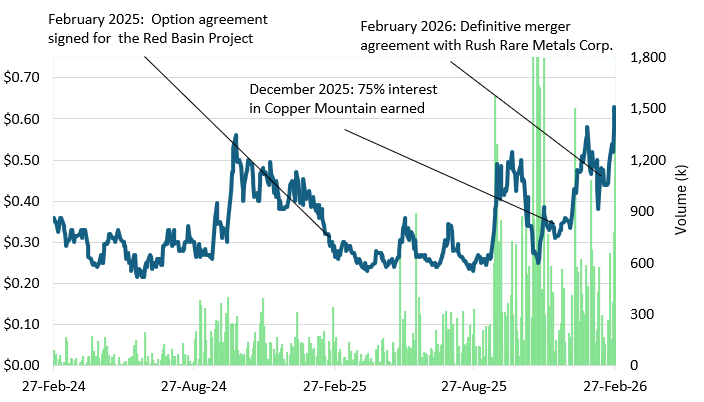

MYRIAD URANIUM (M): IS COPPER MOUNTAIN THE NEXT LARGE SCALE US URANIUM DEPOSIT ?

Copper Mountain consolidation is finally getting done. According to the Definitive Agreement announced with Rush Rare Metals (RSH) last month, Myriad will acquire all of the Rush shares by issuing one Myriad common share for every 1.85 Rush shares issued and outstanding, resulting in an exchange ratio of one (1) Rush share to 0.5405 Myriad shares. Both respective boards are supportive of the transaction. It is well understood that Myriad having 100% ownership of the Copper Mountain Project will greatly simplify and streamline ongoing exploration, permitting initiatives and the overall decision making process with regards to the Project’s future development and strategy. Recall that as announced in December, given the exploration spend to date, Myriad successfully earned 75% ownership of the Project, with Rush owning the balance. A special meeting of Rush shareholders to approve the announced Definitive Agreement is expected to take place in or before May 2026.

Following a maiden drill program which concluded in late 2024 (the first of any such drilling campaign conducted at Copper Mountain since 1979), Myriad management remains busy planning for the next drilling campaign which will include confirming historic drillholes and performing some targeted exploration on the Copper Mountain Project in Wyoming. Building upon an extensive database comprising of over 2,000 boreholes and encompassing a combined ~900,000+ feet of historic drilling, Myriad is in the midst of planning for an upcoming confirmation/exploration program with the intent to bring the historic Copper Mountain resource to current day NI43-101 compliance. Studies conducted between the late 1970s-early 1980s have estimated the resource to be between 15.7M-30.1M lbs U3O8. Other estimates have suggested resource potential upwards of several hundred million lbs U3O8. Since a maiden drill program was conducted in 2024, Myriad management has been working diligently to confirm the historic resource while also conducting targeted exploration. With future drilling currently being planned for, we expect the Project to continue to de-risk while an eventual NI43-101 compliant resource may have the potential to officially rank Copper Mountain as one of the larger uranium deposits located in the United States.

Large Historic Resource at Copper Mountain

Rocky Mountain Energy Corporation (RMEC) estimated Copper Mountain’s resource estimate potential to be as high as 63.8M lbs when factoring in “just” 2 of the 5 identified deposits (Canning and Fuller). At a 0.01% eU3O8 grade cut-off, the resource estimate from the Canning pit alone was estimated to be 21.1M lbs U3O8. In 1980, Fluor followed-up with a study of its own (commissioned by RMEC) in what was considered to be a much more conservative estimate due to the methodology used - conditional lognormal probability distributions. Using the chosen conditional probability, Fluor applied a delayed fission neutron (DFN) adjustment which reduced the grades. Ultimately, an estimate of 14.6M lbs was calculated for Canning and parts of four other surrounding deposits (Fuller, Mint, Allard and Hesitation). Using both the RMEC and Fluor data, further studies were conducted with Gregory Liller authoring a resource estimate in 1991 and A.C.A Howe International Ltd (authored by Bojan Zabev) completing its own resource estimate in 1997. Incorporating the Canning deposit along with portions of 6 other deposits (Fuller, Mine, Allard, Hesitation, Arrowhead and Gem) these two latest reports were summarized as seeing the total resource between 15.7M lbs-30.1M lbs U3O8. For additional details, refer to our initiation of coverage report, dated August 8, 2025.

Recapping Our Investment Thesis

What gives Myriad a big head start with regards to developing Copper Mountain is the substantial project de risking already achieved by way of its historic drilling program. This historic drilling program (conducted in the late 1970s) provided a vast array of technical data which lead to numerous technical reports and various resource estimates derived from different methodologies. In short, the substantial historic work conducted on the Copper Mountain Project has amounted to: A) C$117M in historic exploration spent (2024 dollars), B) 2,000 historic boreholes drilled on the property (totaling ~900,000+ ft), C) A total of 7 deposits discovered and D) Numerous technical reports & resource estimates. In addition to the historic work completed on site, other company positives include:

Location: Wyoming is known to host the large uranium reserves in the United States. The state’s tier-1 uranium status is also accentuated by the fact that nearly a dozen uranium operations are currently licensed. Moreover, uranium mining is currently being conducted at four separate facilities: Ross CPP, Smith-Ranch highland, Nichols Ranch and Lost Creek. Lastly, Wyoming is home to one of the largest uranium mills in the US – currently on standby, the Sweetwater mill has a capacity for 3,000 tpd.

Current Drill Program Success: Myriad’s recently completed 34 hole drill program has returned better than expected grades when using spectral gamma detection. From the assay results received thus far, uranium grades have been 20%-60% higher than the initial gamma probe readings. Additionally, strong grades were detected at depth- this provides for the potential to find deeper target zones.

Copper Mountain Ownership & Land Consolidation Fast-Tracked: In January 2025 Myriad announced the expansion of the Copper Mountain project area, going from approximately 4,200 acres to the current 9,320 acres. Acquired by staking, most of the newly added areas contain historically confirmed uranium mineralisation at surface or subsurface. Myriad exercised its initial 50% option on Copper Mountain by way of meeting the necessary qualifying spend in October 2024. By the end of 2025, 75% of the Project was owned. Given the announced Definitive Agreement, we expect 100% consolidation in the next few months.

Conclusion & Valuation

Seeing as the recent assay results have largely surpassed grades as estimated from gamma probe testing, the potential to confirm the historic resource is apparent, but so is the potential to expand and grow the resource as well. We look forward to the successful consolidation of the Copper Mountain Project and the start of the 2026 drilling campaign. Pending positive drilling success, the risk remains on the upside for a continued valuation re-rate higher.

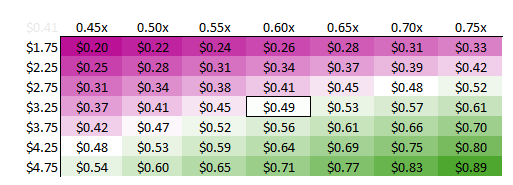

We look forward to the eventual transaction close so that management can focus squarely on maximizing value with the upcoming Copper Mountain drilling campaign. Using the historic resource as a weighted benchmark, we continue to apply our $3.25 per lb in-situ valuation along with a target NAV multiple of 0.60x. We maintain our in-situ based price objective (12 months) of C$0.62 per share. Given that shares have increased by +65% YTD, this equates to potential upside of +2% from the most recent close on February 27. Our most recent note dated February 12, 2026 can be found here.

COPPER FOX METALS (CUU): UPDATED PEA UNDERWAY AT THE VAN DYKE ISR COPPER PROJECT

On the back of a recently closed financing, positive momentum continues with both flagship properties – Van Dyke in Arizona and Schaft Creek in British Columbia’s Golden Triangle. As announced last December, a road map strategy was unveiled to advance the wholly-owned Project to the Pre-Feasibility Study (PFS) stage. Building on the 2020 Preliminary Economic Assessment (PEA), a decision was taken to incorporate a multitude of technical studies and drilling results completed since 2021 to update and optimize the PEA. This optimization work is expected to refine the timeline and fine tune the estimated costs and return metrics for the PFS Execution Plan. At Schaft Creek, the 2026 budget is expected to be announced in the weeks ahead. Significant drill results were announced in January, in an area 500m south of the modeled Liard zone, thus expanding the porphyry footprint. Being one of North America’s largest undeveloped porphyry copper deposits, the PEA-level Schaft Creek Project has garnered much more interest of late given the recent Canadian shareholder and regulator approval for the Teck Resources-Anglo American mega-merger. The combined company has pledged to invest $3.2B in Canada over the next 5 years. With over $100M already invested by Teck in the project, the Schaft Creek JV (75% Teck, 25% Copper Fox) represents one of Teck’s most promising, large-scale polymetallic (copper-gold-molybdenum) projects.

Van Dyke: On the Pathway to a PFS-Level Project

Following a 2020 PEA, management recently updated plans to follow various recommendations laid out in the PFS Execution Plan for Van Dyke. Potentially locating additional hydrogeological monitoring and water sampling stations would support in the development for updated hydrogeological models which would be used to better predict solution flows and potentially projected copper recoveries during the leaching process. Much technical progress has been achieved since the 2020 PEA, among others:

The establishment of four hydrogeological monitoring stations and initiated water quality sampling in accordance with Federal and State regulatory requirements.

Updated conceptual hydrogeological, geometallurgical, geological, structural, and mineralogical models for the deposit.

Preliminary characterization of the copper mineralogy in the oxide and transition mineralogical domains within the deposit.

Preliminary characterization of the copper mineralization, gangue, and host rock to mitigate potential operating issues during the leaching process.

Geotechnical study to determine rock strength and geotechnical characteristics of the Gila Conglomerate.

Infrastructure reviews to minimize environmental and social disturbance.

An Execution Plan outlining expected activities, estimated costs, timeline and permitting process to achieve a PFS level technical report.

Collection of hydrogeological data is currently being sampled daily along with groundwater sampling. The preparation of a 3D numerical groundwater flow model is ongoing.

Recapping Our Investment Thesis

Within Copper Fox’s portfolio we see an enviable mix of advanced, large-scale projects (with both Schaft Creek and Van Dyke having extensive work completed post-PEAs) along with highly prospective projects which can all benefit from additional high-impact drilling campaigns (Eaglehead, Sombrerro Butte and Mineral Mountain). There are currently active programs being executed on all of the portfolio projects.

North American Focused Portfolio: Over the last decade+, Copper Fox has acquired and developed a portfolio of copper projects located exclusively in British Columbia and Arizona. To date, the company boasts projects which encompass 3.00B lbs of copper in the M&I category and 2.34B lbs in the Inferred category (or 4.35B lbs CuEq M&I and 2.98B lbs CuEq in the Inferred category). Of the five portfolio projects, Van Dyke and Schaft Creek both have established Preliminary Economic Assessments while Eaglehead has an established NI43-101 compliant Mineral Resource Estimate.

ISR Exposure at Van Dyke: In light of positive developments in the Arizona SX/EW copper space (from both ISR and heap leach projects) as seen from Florence (Taseko Mines), Gunnison/Johnson Camp (Gunnison Copper) and Cactus (Arizona Sonoran), an updated PEA for the Van Dyke Project is ongoing. Pending certain hydrogeological, mineralogical and solubility studies, a formal decision to advance the project to the PFS level is our expectation, with an eye to an eventual re-start of production.

Strategic JVs: With the Teck Resources – Anglo American merger of equals advancing (Canadian approvals previously granted in December), Teck (as 75% JV partner and operator at Schaft Creek) will decide on the 2026 budget in the weeks ahead. Given over $100M invested by Teck into the Project, our expectation is for an eventual decision to advance the Project to the PFS stage.

Conclusion & Valuation

Copper Fox shares have already started to re-rate higher this past December when Canadian shareholders and regulators approved the Teck resources – Anglo American mega merger. Though approvals are still pending from other jurisdictions, we ultimately expect the deal to close in due curse. Additional near term drivers remain the announced 2026 budget for Schaft Creek and any incremental data from the work being done on updating the Van Dyke PEA.

Shares of Copper Fox currently trade at attractive levels versus peers: at a 0.21x P/NAV valuation and at an EV of C$0.02 per booked CuEq lbs. Our price objective of C$1.05 per share (rounded) equates to upside of +48% from the most recent close (February 27). Our most recent note dated January 26, 2026 can be found here:

FORTUNE BAY CORP (FOR): ADVANCED STAGE PROJECT WITH EXCELLENT GOLD PRICE LEVERAGE

Earlier in February we initiated coverage of Fortune Bay Corp. Though still very much under the radar, we are excited with Fortune Bay’s prospects this year and note that 2026 will be the first year in which the company should potentially re-rate to being viewed as a pure-play gold company with an advanced-stage project working towards PFS completion by year-end. Recall that in previous years, the company was considered as a uranium exploration company focused primarily on the Murmac uranium Project located in the Athabasca Basin (since optioned out). We expect material news flow to trickle out concerning the winter drill program at Goldfields. With a PFS expected to be competed by year-end or Q1/2027, we would expect this company to re-rate to similar valuation metrics as seen with its North American peer group.

Historic Production With Plenty of Historic Work Completed

Located in northern Saskatchewan, the Goldfields Project produced 64,000 gold ounces until the early 1940s. The Project is highlighted by the Box and Athona deposits, located 2km apart, share many similarities which suggest a close genetic association. Mineralization characteristics at Box and Athona are similar, comprising quartz vein sets hosted within a metamorphosed and hematized leucogranite, respectively termed the Box and Athona “Mine Granites”. The Project lay dormant until the 1980s when trenching, prospecting, metallurgy sampling and resource delineation was re-started on site. more recent work on site involved drill testing targets at Box, Athona, Frontier Lake and Triangle. Up until 2011, historic drilling at Athona totaled 376 drill holes totaling 29,077m while at Box, historic drilling amounted to 552 drill holes totaling 67,108m.

Recent Drilling

As per more recent drilling by Fortune Bay, 18 holes (6,946m) were drilled at Goldfields between January 2021-March 2022. The drilling was focused at Athona and Box. The program was specifically designed to expand the mineralization footprints beyond the historical drilling coverage, and to commence delineation of additional mineral resources. Post-drilling, a total of 3,036 samples were collected and submitted for gold assay and analysis. Highlight assays from both Athona and Box included:

A21-218: 3.0m grading 3.60 g/t Au from 115.0m to 118.0m (Athona)

A21-221: 2.0m grading 1.57 g/t Au from 32.0m to 34.0m (Athona)

A21-223: 19.0m grading 1.22 g/t Au from 92.0m to 111.0m (Athona)

B21-334: 8.0m grading 4.38 g/t Au from 286.0m to 294.0m (Box)

B21-335: 36.0m grading 1.34 g/t Au from 312.0m to 348.0m (Box)

B21-338: 19.0m grading 1.42 g/t Au from 413.0m to 432.0m (Box)

All samples from Box and Athona were incorporated into the mineral resource estimate. From Athona, holes A21-219, A21-220 and A21-222 all intersected mineralization, demonstrating expansion of Athona to the south. Drill holes A21-218 and A21-221 intersected grades and mineralization characteristics consistent with those observed within the Athona Main deposit, suggesting continuity between Athona Main and Athona South.

The latest NI43-101 compliant Mineral Resource Estimate models published last year (replacing the MRE with an effective date of October 31, 2022) included a total of 838 boreholes, of which 494 are located within the Box deposit and 344 within the Athona deposit. Gold grades were interpolated into the block models using ordinary kriging (OK) for all granite and vein-set domains within the Box and Athona deposits. Grade estimation for each domain was conducted using multiple passes, with successively expanding search criteria in subsequent estimation passes.

Ultimately, both the Box and Athona deposits remain open at depth. Exploration drilling began this past November at the Box deposit with 3 holes completed totaling 1,125m. At Box, current drilling is focused on down-dip step-outs (200m-350m) into significant gaps in drill coverage within and below current Inferred Mineral Resources, well outside of the mine pit outlined in the updated PEA. A total of 17 drill holes (3,250m) are in process for this winter split between Box (4 total holes) and Athona (2 holes). Additionally, exploration drilling will also focus on targets such as Frontier (3 drill holes planned for), Golden Pond (six holes) and Triangle (2 holes).

PEA Economics

Given a forecast 4,950 tpd throughput, the mine life was calculated at 13.9 years including 11 years of direct mill feed from pit operations and subsequent low-grade stockpile rehandling. Over the entire project LOM, total payable gold production was estimated to be 896,000 ounces, or 64,300 ounces per year on average. Factoring in a cash cost of $1,207 per ounce ($1,330 per ounce AISC), initial capex of C$301.1M and sustaining capex of C$142.5M, (among others). Using a base case LT gold price deck of $2,600 per ounce, an after-tax NPV5% of $913.7M was calculated, along with an after-tax IRR of 44%. At a LT gold price of $3,650 per ounce, the after-tax NPV5% amounted to $1,253M while the after-tax IRR totaled 74.2%.

Conclusion & Valuation

With a PFS expected to be competed by year-end or Q1/2027, we would expect this company to re-rate to similar valuation metrics as seen with its North American peer group. Given the most recent close (February 27), shares of Fortune Bay trade at a 0.06x P/NAV valuation, or at $58 per global Au ounce – well below that of peers. For more information refer to our February 4, 2026 initiation of coverage report. Link below.

Given the most recent close (February 27), shares of Fortune Bay trade at a 0.06x P/NAV valuation, or at $58 per global Au ounce – well below that of peers. Our price objective of C$3.15 per share (rounded) equates to upside of +258% from the most recent close (February 27). Our most recent report dated February 4, 2026 can be found here:

PREMIER AMERICAN URANIUM (PUR): CREATING ONE OF THE LARGER US URANIUM PURE PLAYS

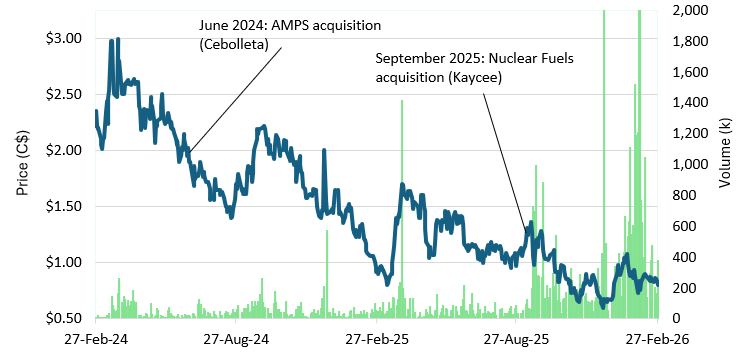

Since IPO on the TSXV in late 2023, significant acquisitions and have defined Premier American’s strategy, on the way to accumulating one of the largest and most prospective uranium portfolios grounded exclusively in the US. Along with the acquisitions, sizeable drilling campaigns have followed - this past January, meaningful exploration results were announced for both key Wyoming assets; the Cyclone ISR Project and the Kaycee ISR Project.

From Cyclone, the conclusion of the 2025 drill program was successful in identifying new zones of mineralization while also identifying a new 1.5 mile trend and extending the previously identified 0.5 mile east-west trend. The data received from this latest drill campaign will set the stage to refine or establish targets for an upcoming campaign to further de-risk and model the uranium resource. From Kaycee, follow-up drilling last year in the Outpost target area confirmed the presence of a newly defined uranium-bearing roll front system within Fort Union Formation channel sands. 8 of the 11 mineralized holes encountered grades of 0.02% eU3O8 or greater with a thickness of at least 2 ft, including 3.5 ft of 0.27% eU3O8 in drillhole LT25-065 and 5.5 ft of 0.125% eU3O8 in drillhole LT25-069. From the Rustler area, 15 of the 22 mineralized holes encountered grades of 0.02% eU3O8 or greater with a thickness of at least 2 ft, including 8.5 ft of 0.083% eU3O8 in drillhole RT25-042.

Portfolio of Projects in all the Best US Uranium Locations: The Four Corners States & Wyoming

Given the acquisition of Nuclear Fuels Inc (closed in September 2025), Premier American has been successful with adding key uranium Projects in top jurisdictions such as Arizona, Utah and most importantly, Wyoming (Kaycee), to its US-focused uranium portfolio. Located in Wyoming’s prolific Powder River Basin, the Kaycee Project hosts a historic uranium resource given that over 3,800 holes were drilled on site mostly in the late 1970s. An NI43-101 compliant technical report was released in 2024. The report highlighted a uranium exploration target between 11.5M-30.0M lbs. The Kaycee Project encompasses nearly 34,000 acres in north east Wyoming. Notable ISR projects located in close vicinity include Nichols Ranch and Hank (both Energy Fuels, UUUU), Irigaray and Christensen Ranch (both Uranium Energy Corp, UEC) and North Butte (Cameco, CCJ).

In June 2024, Premier acquired the Cebolleta Project, located in New Mexico. An extensive work program quickly followed, culminating with the publication of a Preliminary Economic Assessment and an updated Mineral Resource Estimate released on October 30, 2025.

The Preliminary Economic Assessment illustrated Cebolleta’s potential for a large scale, heap leach operation which would produce an average of 1.4M lbs of uranium resin suitable for off-site processing, over a an estimated LOM of 13 years. Specifically, the Cebolleta process design incorporates average daily throughput of 2,300 tpd, average U3O8 head grades of 0.11% (over LOM) and heap leach recovery of 80%. The updated MRE increased the Indicated resource estimate by 1.7M lbs eU3O8 (+9%) to 20.3M lbs while the Inferred resource estimate increased by 2.2M lbs eU3O8 (+45%) to reach 7.0M lbs. This revised resource (effective day May 15, 2025) updates the previous estimate released in the April 2024 Technical Report.

Recapping Our Investment Thesis

With Premier American we see a pure-play, US-focused exploration/development play active in all the best uranium jurisdictions. Management has shown its willingness to make transformative acquisitions while also following up with robust development plans. Not only does the company rank as one of the largest in terms of US project portfolio, but with ~117,000 ft drilled in 2025, it also ranks as one of the most active drillers in the space.

Diversified Uranium Project Portfolio – With substantial acreage in each of the Four Corners’ states and Wyoming, the company boast established or prospective projects in some of the best uranium jurisdictions.

Diversity of Projects – The current portfolio boasts PEA level Projects (Cebolleta), along with Projects such as Kaycee and Cyclone which encompass recent Technical Reports and accompanying exploration targets.

Aggressive Development Timeline – If the past should be any indication of what is to come, we can only assume that further project acquisitions may materialize over the course of 2026. With even greater certainty, we can expect robust drilling campaigns spread over the entirety of the portfolio. With a recent C$15M financing closed (February 3, 2026), we can expect further development work on the flagship Wyoming and New Mexico projects.

Conclusion & Valuation

We maintain our C$1.73 per share price target. This equates to upside of +116% from the February 27 close. Shares of Premier American Uranium currently trade at a P/NAV of 0.35x. Our most recent report dated January 14, 2026 can be found here:

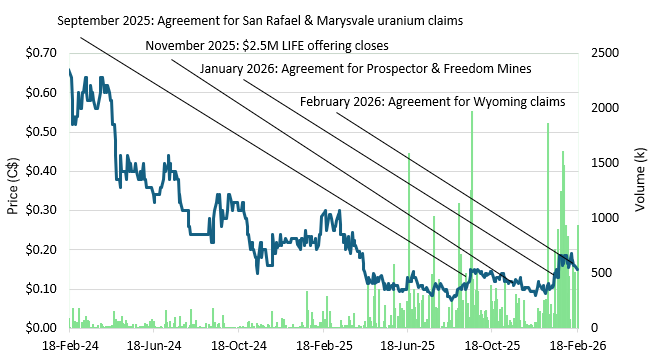

TERRA CLEAN ENERGY CORP (TCEC): STRATEGIC NEW UTAH/WYOMING URANIUM ACQUISITIONS

Over the last few months, Terra management has been active in re-shaping the company by spearheading a concerted effort to add strategic US uranium Projects in order to diversify from being solely an Athabasca Basin focused uranium company. With a recent financing closed, successful staking/acquisitions in Wyoming and two recent Utah earn-in agreements finalized, given the compelling re-focus of the company, we re-launched research coverage earlier in February.

Last September, Terra announced its entry into Utah by way of an earn-in agreement for 75 uranium claims located in Emery County. This news was followed up this past January with the announcement of another earn-in agreement encompassing six Bureau of Land Management (BLM) unpatented Lode Mining Claims located in Piute County, Utah. Both claim areas are strategically located within 150 miles of the White Mesa Mill (owned by Energy Fuels, UUUU) and the Shootaring Canyon Mill (owned by Anfield Energy, AEC). Both claim areas contain numerous near surface, past producing, uranium mines. Just as importantly, management has also secured numerous historic technical reports conducted on the properties, these reports will be used as the basis to formulate and eventually coordinate the first targeted drilling program seen on the properties in 50+ years.

As announced earlier in February, by way of staking and State lease acquisition, a total of 3,395 acres in Wyoming were added to the company’s current portfolio of prospective uranium properties. Situated near the Colorado state border, the contiguous land package in the southern flank of the Washakie Basin is located in close proximity to enCore Energy’s (EU) Juniper Ridge uranium deposit and Homeland Uranium’s (HLU) Coyote Basin Project. With these latest property acquisitions and with the earn-in agreements in place, Terra now boasts a diversified portfolio of uranium properties located in some of North America’s premier uranium districts – the Athabasca Basin (South Falcon East), the Marysvale Uranium District (Prospector & Freedom Mines), the San Rafael District (San Rafael West) and the Washakie Basin (Wyoming Claims). With a financing closed last November, the stage is set to re-examine the historic data and plan for a high impact drilling program. Next month, prospecting, trenching and mapping will commence at the Prospector & Freedom claims. Permitting for a 10,000ft drilling program will also commence in March. Drilling is ultimately planned to begin in May/June.

Green Vein Mesa & Wheal Anne Claims – Historic Production & Plenty of Historic Data

As announced on September 16, 2025, Terra management negotiated an earn-in agreement for 75 uranium claims in the San Rafael Swell. The San Rafael Swell is a large, uplifted, doubly-plunging anticline in east-central Utah and the Swell forms part of, but contrasts with the surrounding flat-lying rocks, of the Colorado Plateau, a significant uranium mining district in the Western United States. Historical uranium production was undertaken in the Swell between the late 1940’s until 1969 when approximately 7.0M lbs U3O8 was produced. No significant work has been completed in the region over the past 50 years. The rocks in the San Rafael Swell are predominately sedimentary (Pennsylvanian through Cretaceous), including Triassic and Jurassic formations which are known to host uranium. The project area is underlain by Triassic aged sedimentary rocks of the Moenkopi and Chinle formations. The Chinle outcrops in a continuous belt around the San Rafael Swell and on isolated buttes through the center of the swell. It is widely believed that volcanic ash is the source of uranium for many deposits in the swell. All existing mines and prospects in the Chinle are in the lower, bentonitic part of the Chinle in channel-fill sandstone and surrounding siltstones of the lower Chinle Formation.

The two claim groups (Wheal Anne and Green Vein Mesa) are located 10km apart. The Wheal Anne Claim Group (16 claims) is the southwest of the two and encompasses approximately 130 hectares covering the former producing Lucky Strike Mine and related uranium occurrences. Historic production from mines contained on both claim groups contributed to approximately 450,000 lbs of uranium production. The Green Vein Mesa claim group (32 claims) is located to the northeast encompasses approximately 300 hectares. The claims cover the former producing Payday Mine, Hertz Mine, and Green Vein group of mines. The Hertz Mine reportedly had local samples up to 1.00% U3O8. Historic production numbers for these mines totaled approximately 400,000 lbs U3O8. The Wheal Anne claim group (16 claims) is highlighted by the Lucky Strike Mine which was discovered in 1949 and historically produced approximately 44,000 lbs U3O8 (10,000 tons grading 0.22% U3O8).

Recapping Our Investment Thesis

On an EV basis, Terra currently trades at a ~70% discount to its US-focused, pre-resource peer group. We feel that this is currently justified given the constraints weighing on the company such as company size and liquidity. Moreover, the new direction positioned towards Utah and Wyoming coupled with the very modest and attainable earn-in conditions remain largely unknown to the market. It is our view that this dynamic will change as the new assets will slowly de-risk as development ramps and milestones are made.

Earn-In Agreements Signed for Utah Uranium Properties – Earlier in January Terra announced plans to earn a 100% interest in the past producing Freedom & Prospector Mines Project, located in Marysvale Utah. This announcement follows the September 2025 announcement that an earn-in framework was negotiated for a 100% interest in past producing uranium claims (the Wheel Anne claims and the Green Vein Mesa claims) located in Emery County, Utah.

Historic Production, Strategic Location – The Utah claim areas include a number of historic mines which collectively produced approximately 1.45M lbs uranium between 1949-1969. Both Utah claim areas are well situated within 300km of either the White Mesa mill or the Shootaring Canyon mill.

Successful Staking in Wyoming – Given low cost staking and lease acquisitions, a sizeable 3,395 acres were obtained in Wyoming. Located in the Washakie Basin, the property package is situated just 75km from historic uranium production in the Poison Basin and 120km from enCore Energy’s PEA-level Juniper Ridge Uranium project.

This is the New Terra Clean Energy Corp. – Though the uranium portfolio continues to contain the 6.8M lb deposit in the Athabasca Basin (South Falcon East), the recent US acquisitions fundamentally change the profile of the company. In our view, the new claim areas and the corresponding capital outlays which we deem as modest and achievable, greatly enhance the profile and future prospects of the company.

Conclusion & Valuation

Given the new Utah & Wyoming focus and the numerous near term development targets, we re-initiate coverage of Terra Clean Energy Corp. and establish a price objective of C$0.30 per share. This equates to upside of +100% from the recent February 27 close. Our most recent report dated February 19, can be found here:

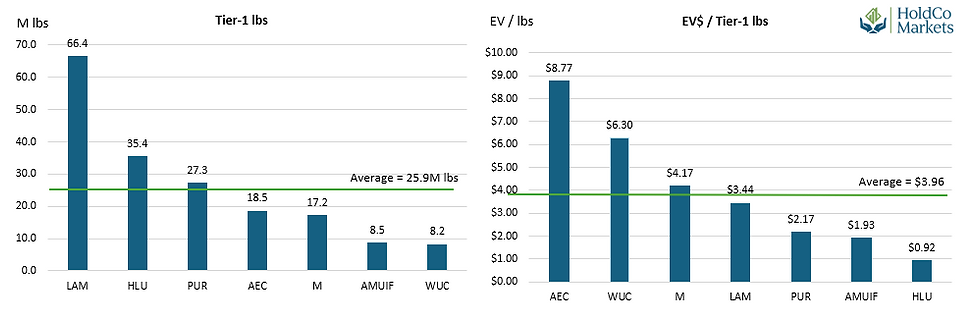

EXHIBIT 1 – PEER VALUATION